BOFIT Viikkokatsaus / BOFIT Weekly Review 2023/46

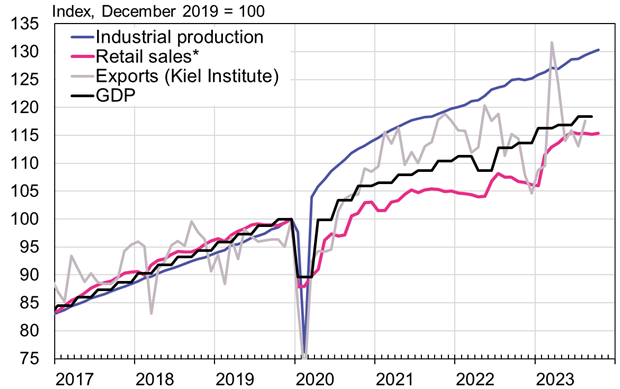

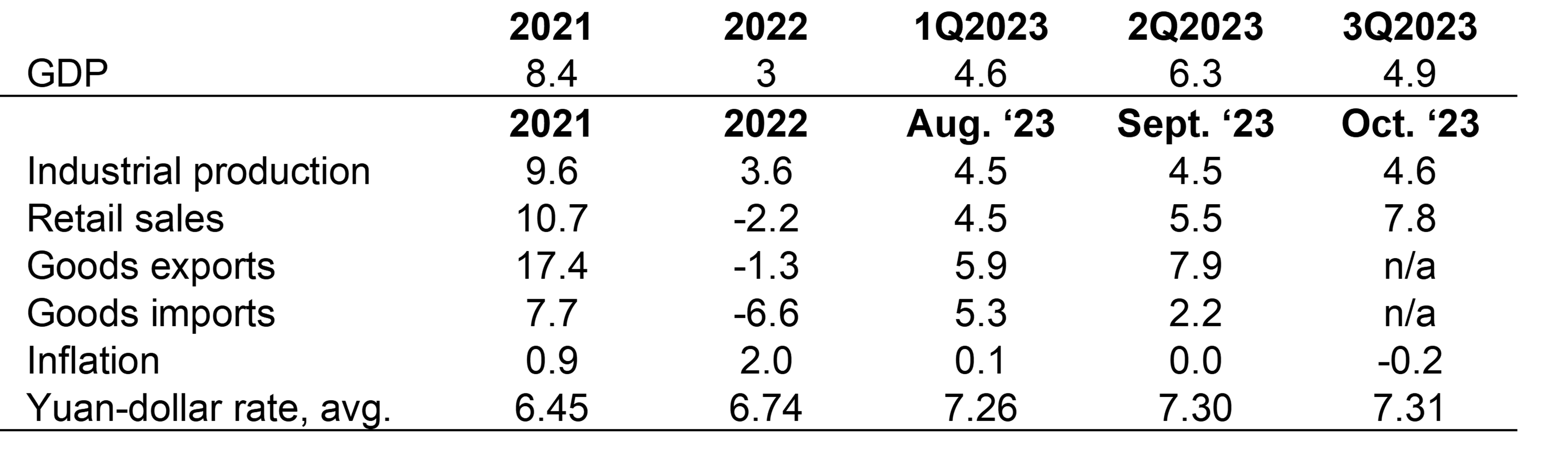

Last month’s economic growth, however, was lower than in pre-pandemic years and recovery from the lifting of covid restrictions remains disappointing. Industrial output was up by 4.6 % y-o-y in October, about the same pace as in August and September. Automobile production (up 11.3 % y-o-y in January-October) has grown faster this year than overall industry, while output of high-tech manufacturing lagged average production growth (1.9 %). The real estate market has yet to show any signs of recovery. The declines in both real estate investment (down 17 % y-o-y) and the volume of housing sales (down 20 % measured by floorspace) continued in October.

Retail sales climbed by nearly 8 % y-o-y in October, but the increase was due mainly to last year’s relatively low basis reference. Compared to the previous month, retail sales growth was marginal. In the retail sales category, restaurants and other services have been the fastest growing sub-item this year. Consumer prices fell in October by 0.2 % y-o-y. This was due mainly to a drop in pork prices (down by 30 % y-o-y in October). Core inflation (excludes food and energy prices) slowed slightly to 0.6 %.

Industrial output has grown faster that retail sales since the first wave of the Covid-19 pandemic

*) Nominal retail sales deflated by the consumer price index.

Sources: China National Bureau of Statistics, Kiel Institute, CEIC and BOFIT.

The value of goods exports in October was down by 8 % y-o-y in dollar terms (down 5 % in yuan). Imports, in contrast, picked up in October, with the dollar value of goods imports rising by 2 % y-o-y (up 6 % in yuan). The development of China’s foreign trade volumes this year has been more favourable than foreign trade measured in terms of value. Prices of both exports and imports have been falling since last spring. According to WTO figures, the volume of Chinese goods exports in the second quarter rose by 2 % y-o-y, but its value declined by 4 %.

On-year growth in China’s broadest debt measure, aggregate financing to the real economy (AFRE), accelerated a bit in October to 9.3 %. Much of the increase was due to bond issues by local governments. Demand for private sector loans is still fairly weak. For example, on-year growth in household loan stock remained at just 3 % in October. Local governments have this year been granted permission to issue a quota of 1.5 trillion yuan (205 billion dollars) in new special purpose bonds to pay off some of their hidden high-interest debt. As of early November, 1.2 trillion yuan in such bonds had been issued.

Real 12-month change and consumer prices, %

Sources: China National Bureau of Statistics, China Customs, WTO, CEIC and BOFIT.

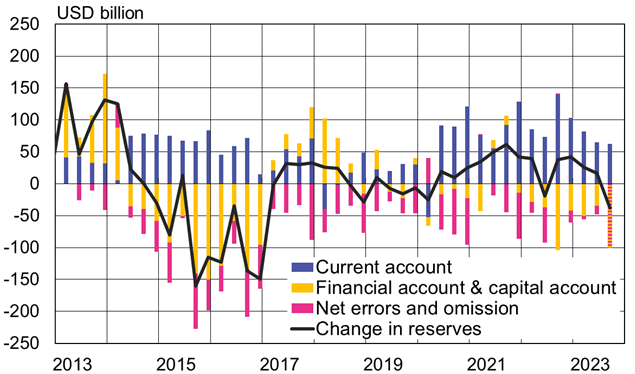

Balance-of-Payments figures show increased capital outflows from China

In its balance-of-payments statement, the People’s Bank of China reports that China’s still large goods trade surplus helps to offset the again growing services trade deficit and that the financial account has shown a deficit for two years running. Additionally, the “net errors and omissions” term in the balance-of-payments remains negative, indicating that more assets are flowing out of China than officials have managed to classify. According to the PBoC’s preliminary balance-of-payments figures, the cumulative goods trade surplus for the first three quarters of this year amounted to 454 billion dollars. The total current account surplus was 209 billion dollars, reduced largely by a growing services trade deficit that amounted to 168 billion dollars in January-September (up from 62 billion dollars in the same period last year). The financial account and net errors and omissions term in the first three quarters of this year showed a combined deficit of 205 billion dollars, suggesting that the level of China’s foreign exchange reserves has been largely unchanged this year.

Among the sub-items in the financial account, however, especially the direct investment flows clearly turned outward. The direct investment balance has been negative (i.e. Chinese direct investment flows outward have surpassed inward foreign direct investment flows) since the end of 2021. For the first nine months of this year, the balance-of-payments data show foreign direct investment inflows to China of 15 billion dollars and an outflow of 143 billion dollars. In the third quarter, the inflows of direct investment into China also turned negative by 12 billion dollars for the first time since China started keeping quarterly balance-of-payments records in 1998. This indicates that foreign firms operating in China in net were seeking to repatriate profits or divest assets in China. Recent surveys of foreign firms operating in China also indicate that the firms have become more cautious with respect to new investment in China and more interested in finding alternative countries for their additional investments. The portfolio investment balance of the financial account was negative last year and in the first two quarters of this year (3Q figures have yet to be released). For the January-June period, Chinese investors made portfolio investments abroad valued at 52 billion dollars, while foreign investors reduced the amount of their holdings in China by 10 billion dollars.

Balance-of-payments net flows turned negative in the third quarter

Note: Financial account, capital account and net errors and omission terms combined for 3Q2023.

Sources: SAFE, Macrobond and BOFIT.