BOFIT Weekly Review 7/2021

Central Bank of Russia keeps key rate unchanged

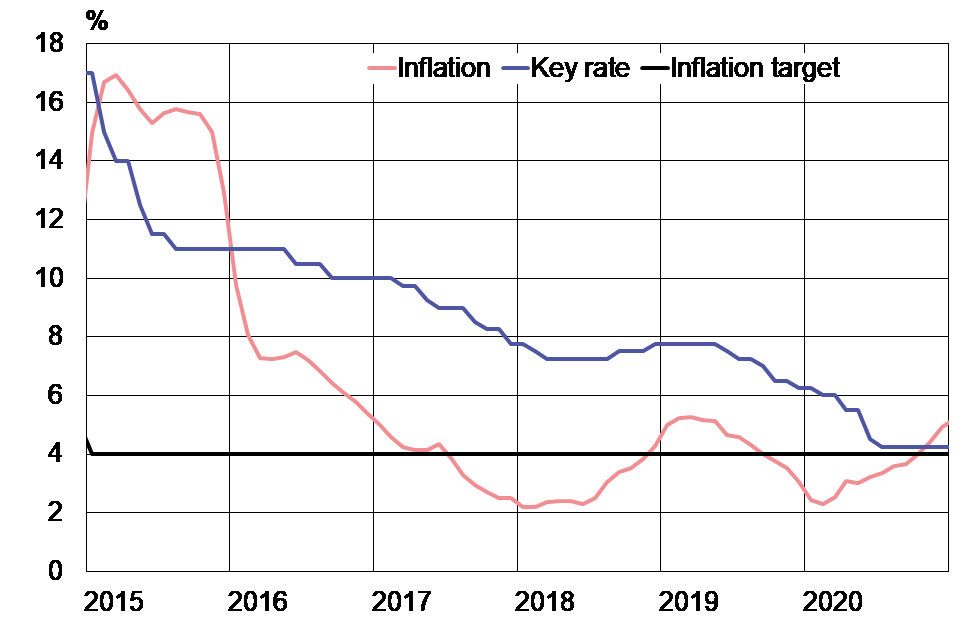

On February 12, the CBR decided to keep the key rate unchanged at 4.25 %. The decision was in line with the expectations of market analysts. The CBR’s key rate has remained unchanged since July 2020.

Consumer prices rose by 5.2 % in January, slightly faster than the CBR’s forecast. Inflation picked up due to such factors as supply-side shocks to the economy from the covid crisis, spikes in certain food prices (BOFIT Weekly 51/2020) and rising inflation expectations on the part of households and corporations. Prices have also been rising due to the ruble’s depreciation since last summer.

The CBR expects inflation to peak this year in February-March. As a result, annual inflation is forecast to reach the range of 3.7–4.2 % (earlier 3.5–4 %) in 2021, after which it should remain close to 4 %. The CBR’s inflation target is 4 %.

Under the updated guidance, the CBR will return gradually from the current accommodative stance to neutral monetary policy (key rate in the range of 5–6 %). CBR governor Elvira Nabiullina noted, however, that monetary policy will remain accommodative on average through this year. Although the Russian economy contracted less than forecast last year (BOFIT Weekly 5/2021), the CBR’s growth forecast of the economy remains unchanged. The forecast sees GDP growth of 3–4 % this year, 2.5–3.5 % in 2022 and 2–3 % in 2023.

Russian key rate, annual consumer price inflation and the CBR’s inflation target Sources: Central Bank of Russia, Rosstat, Macrobond and BOFIT.

Sources: Central Bank of Russia, Rosstat, Macrobond and BOFIT.